The Islamic Case for Bitcoin

This is an opinion editorial by Muslim Bitcoiner, the host of the Muslim Bitcoiner Podcast. This content is for informational purposes only and does not represent legal, tax, investment, financial, or other advice.

One of the biggest challenges Muslims face when seeking to invest in a halal way is to avoid Riba. For this article, we define Riba as any amount of interest charged on a loan, which is strictly prohibited in Islam. Muslims who aim to avoid this sin spend an enormous amount of time sifting through various financial instruments to do simple things like buy a car or house. Even more time and effort are spent for those who invest, as it can be time-consuming to find shariah-compliant investments. And finding a bank that allows you to store your cash (without it being lent out to earn interest for the bank) is almost impossible.

The reality is, for most Muslims, spending this time and effort isn’t feasible. It takes hours of reading and learning sophisticated financial jargon to navigate the stock market properly. With work, kids, prayer, and other responsibilities, the average Muslim doesn’t have time to spend researching and acquiring this knowledge.

For the small percentage of Muslims who go down the “halal investor” path, refining investments to pass shariah compliance can be a long and complex process. Fortunately, we now have an app like Zoya that provides an easy solution to screen your investments for shariah compliance, simplifying the process for Muslims.

Halal Stock Screener & Portfolio Tracker

Zoya makes halal investing easy by helping you build and monitor a shariah compliant investment portfolio with confidence and clarity.

However, I have found that the average Muslim still finds it tedious to get involved with halal investing due to the amount of time and effort that is required to navigate the financial space. This leads them to saving cash in a bank account, which involves more Riba than investing in stocks (more on that later).

But can our wealth truly be 100% halal if we put in enough effort? This is the question that every Muslim needs to investigate and ponder. After all, no Muslim wants to partake in Riba. I believe that it is almost impossible to have our wealth be halal within our current monetary system. Let’s explore this.

Riba in the current monetary system

Have you ever wondered how money and banking actually work? Allow me to explain.

When money is deposited at a bank, the money isn’t actually held there. The bank operates as a fractional reserve, meaning they are only required to hold a certain reserve of dollars and can loan up to 10 times or more (here is a helpful video explaining how this works).

Let’s say Ahmad deposits $100 at a bank. If the bank has a reserve requirement of 10%, then the bank only needs to keep $10 in reserve and can loan out the other $90. Now keep in mind that Ahmad can still withdraw his entire $100 from the bank whenever he wants so that loaned $90 has technically been created from nothing. Now consider that that loaned $90 finds its way back to the bank. Again, under a 10% reserve requirement, the bank only needs to keep $9 and can subsequently loan out $81. If we keep iterating, we see that the original $100 deposit made by Ahmad enables the banks to create $1,000.

All of these loans enabled by Ahmad’s deposit are tied to interest. This “money multiplier” effect points to a bigger problem. All dollars are created through interest. Tarek El-Diwany explains this in his book The Problem with Interest:

"Bank money cannot be created other than by a loan, and therefore almost inevitably bears interest as a condition for its existence."

Let’s dig into this a little further. In the previous example, we used a 10% reserve requirement to illustrate how fractional reserve banking works and how lending creates more money. Historically speaking, 10% is a typical reserve requirement for banks. However, as of March 2020, the Federal Reserve has set the reserve requirement to 0%. This means that banks are legally not required to keep any cash in reserve. So the money multiplier effect can now allow for infinite interest-bearing lending, i.e., money creation by the banks.

So we’ve covered how dollars are created at banks, but how are dollars made at the Federal Reserve level? When the Federal Reserve wants to inject money into the supply, it goes to the ‘open market’ to buy treasury bonds and creates dollars to purchase them. Treasury bonds are just debts that bring in interest to the owner.

The Federal Reserve must enter the open market to buy and sell debt securities to manipulate the money supply. Now the Fed isn’t just manipulating the money supply arbitrarily; it does so to target an interest rate. If the Fed wants to lower the interest rate, it will inject more money into the supply by buying treasuries. To increase the interest rate, it will destroy money in the supply by selling treasuries.

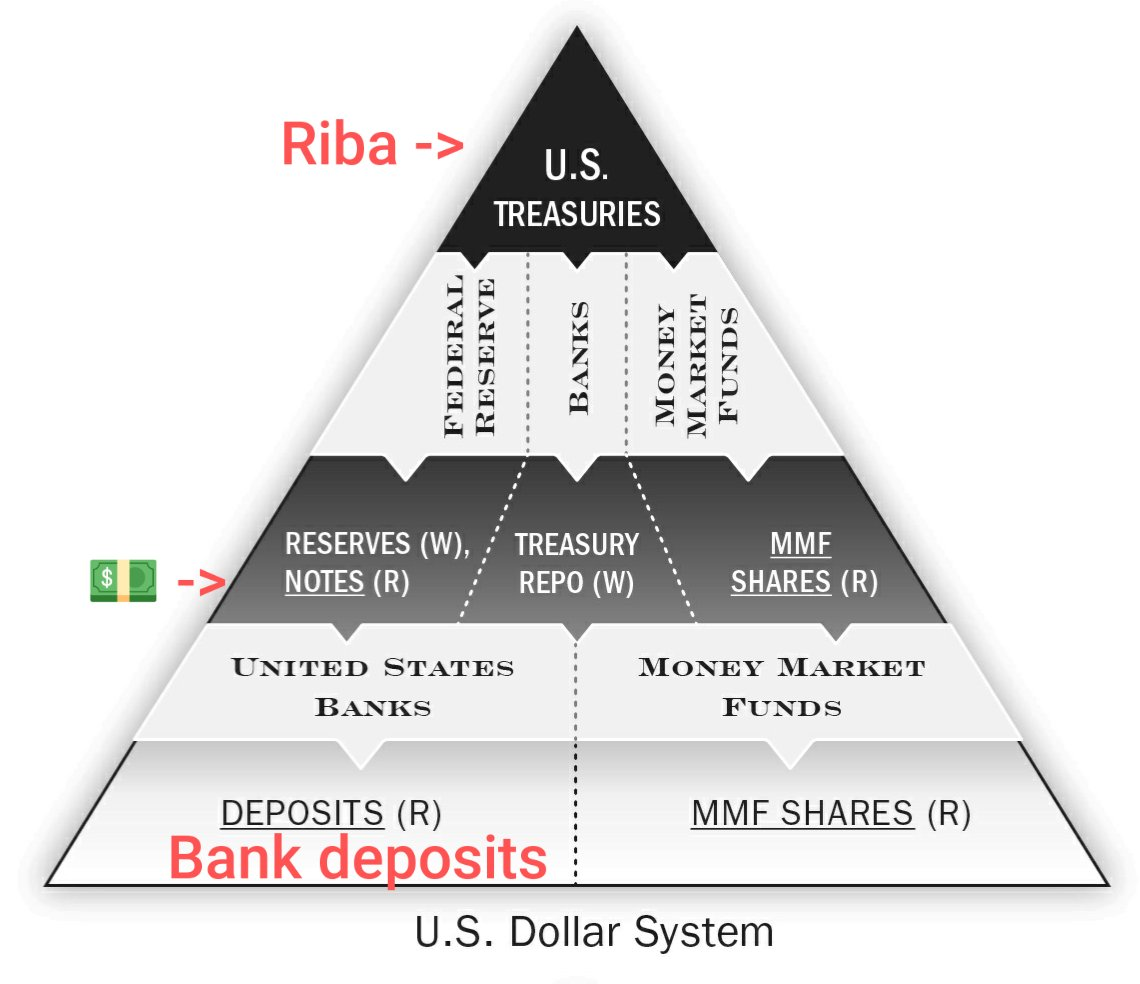

In essence, the US treasury bill is the foundation of the global financial system. It is important to remember that US Treasuries are what back the dollar, which is fundamentally interest-bearing debt. Let’s think of money in the current monetary system in hierarchies. Treasuries are at the top layer, which is the strongest and least risky form of fiat money, as illustrated in this graphic from Nik Bhatia’s book Layered Money.

The main takeaway from this graphic is that the current global monetary order depends entirely on Riba to work.

Now that we’ve established that Riba is inextricably linked to the dollar, the question arises: How can we avoid Riba given the current nature of fiat money?

We can invest in companies and funds that pass shariah compliance, which may be enough for some Muslims to have a clear conscience. However, shouldn’t we consider that maybe we must come up with or flee to another monetary system entirely? Is there a technology that Muslims could use to help us escape Riba once and for all?

I argue that Bitcoin is the most effective way for Muslims to escape Riba. In this sense, Bitcoin is the most halal form of money since it is the perfect anti-Riba monetary technology.

Bitcoin as anti-Riba technology

I won’t get into the technical aspect of how Bitcoin works, as many of you will have already heard of Bitcoin (check this and this out to learn more about what Bitcoin is). However, as a Muslim, it is essential to grasp that Bitcoin is a new type of money (not just a fiat investment vehicle or payment application) that possesses this overlooked “anti-Riba” property. Let’s review some key attributes of Bitcoin that will help us understand the anti-Riba technology embedded in the Bitcoin protocol.

Bitcoin has a fixed supply cap of 21 million. This means there will only ever be 21 million Bitcoin (BTC). Anyone with a cheap laptop or computer with an internet connection can participate on the Bitcoin network to verify this supply cap. Only about 19 million BTC have been mined to date, which leaves 2 million bitcoins left. At first glance, this may seem like an inadequate supply for global adoption, but each bitcoin is highly divisible into smaller units.

Without getting too technical, mining involves expending energy in the real world and providing proof that this work was done to process transactions. This process of expending energy in the real world and providing that proof to secure the Bitcoin network is called proof-of-work.

Miners bundle transactions into a block, then it is added to the blockchain, which is the entire record of Bitcoin transactions. But before the new block can be added, it must be validated and authenticated by providing a unique number based on the parameters of the previous block. Miners must use specialized computers to try billions of guesses per second to find that unique number. Miners receive bitcoin for their service as a reward for participating in this “proof-of-work” competition. This process is the only way for more Bitcoin to enter the supply of existing Bitcoin. This system cannot be cheated whereby someone can just conjure Bitcoin from nothing.

Let’s contrast this with the Riba-based fiat system. In order to ‘mine’ fiat, the Federal Reserve and commercial banks need to issue debt instruments, either in the form of buying treasuries or through issuing a mortgage. All of this debt is tied to Riba. Banks are supposed to be irresponsibly leveraged and are rewarded for making risky loans. If a bank goes bankrupt, there is a “lender of last resort.” The Fed will loan out more money to keep these banks functioning, and these banks will then loan out more money, increasing the money supply. Interest is inherently tied to the entire process of ‘mining’ fiat.

As you can see with Bitcoin, there is a hard cap of 21 million, and there is no central authority that can change numbers on a database to create more money or manipulate interest rates. Under a Bitcoin standard, money is verifiably stored on a ledger and is not loaned to create more money with interest.

Hypothetically speaking, two people can still transact in a Riba-based loan using BTC, but this happens in a closed system. If Alice loans Bob 1 Bitcoin at a 10% interest rate, Bob pays back 1.1 Bitcoin at the end of the loan period. This transaction doesn’t affect me or you or anyone that’s holding Bitcoin. There is no monetary inflation as a result of this Riba-based transaction. Bob and Alice can directly conduct this transaction without it impacting the supply of Bitcoin on the network.

Because of the energy requirement and hard supply cap, I suspect that lending for the sole purpose of earning interest will drastically diminish under a true Bitcoin standard. Logically speaking, it wouldn’t make sense for someone to lend out their Bitcoin for a small upside of earning a measly amount of interest with the huge downside of losing the entire amount of loaned Bitcoin?

Central banks can’t just print more Bitcoin in the case of a default. Therefore, solely profiting from interest becomes inherently riskier under a Bitcoin standard. Investors are more likely to lend Bitcoin to invest in businesses that will yield profit greater than the rate at which Bitcoin will appreciate. Lenders will be forced to make sound and economical loans because if the borrower defaults on the loan, there is no “lender of last resort” that can create more Bitcoin from nothing. This is how a sound monetary system should operate, in my opinion. Loaning should only be used for investing in businesses and not just for earning interest, and this is precisely what Islamic finance and economics promote.

Getting off of zero Bitcoin

It’s understood that Riba is one of the worst sins that we can engage in as Muslims, so it’s imperative that we attempt to make our wealth as “Riba-free” as possible. The first step in doing so is to acknowledge that Riba is at the heart of our global financial system, and that we must strive to break free from this.

I believe that Bitcoin could be a part of the solution to the malevolence of Riba. There are many reasons to hold Bitcoin, but as a Muslim investor, holding Bitcoin as a truly anti-Riba investment is perhaps the best reason.

I’m not suggesting that investing in stocks or other financial assets is entirely haram and that you should go all in on Bitcoin. However, if you are sincerely trying to make your portfolio as halal as possible, then you may want to consider dipping your toe in and learning about this new monetary technology.

The point is to get off of zero Bitcoin. Due to its anti-Riba properties, Bitcoin should be a staple as the halal asset every Muslim should own.

A new foundation is needed for Muslims to address the Riba problem effectively. Bitcoin could be that foundation to help cleanse our portfolios from the filth of Riba.