Yeni Başlayanlar İçin Sukuk Rehberi

It is common for conventional investors to talk about diversifying their portfolio, often referring to a stock-to-bond split. What does this mean, and is this something you should consider as a Muslim investor? These investors are referring to the percentage of stocks and bonds they hold in their portfolios. The typical advice for those investors is to allocate a higher portion of stocks if you are younger and a higher percentage of bonds if you are older.

Stocks are inherently riskier assets to invest in, so younger people would have more time to recover from a short-term drop in value and benefit from potentially higher returns. Someone older or closer to the end of their investment horizon would be better off having a more significant chunk of their investments in an asset with more stable returns. Let’s dive into how bonds work and how they can provide a predictable income stream.

What are bonds?

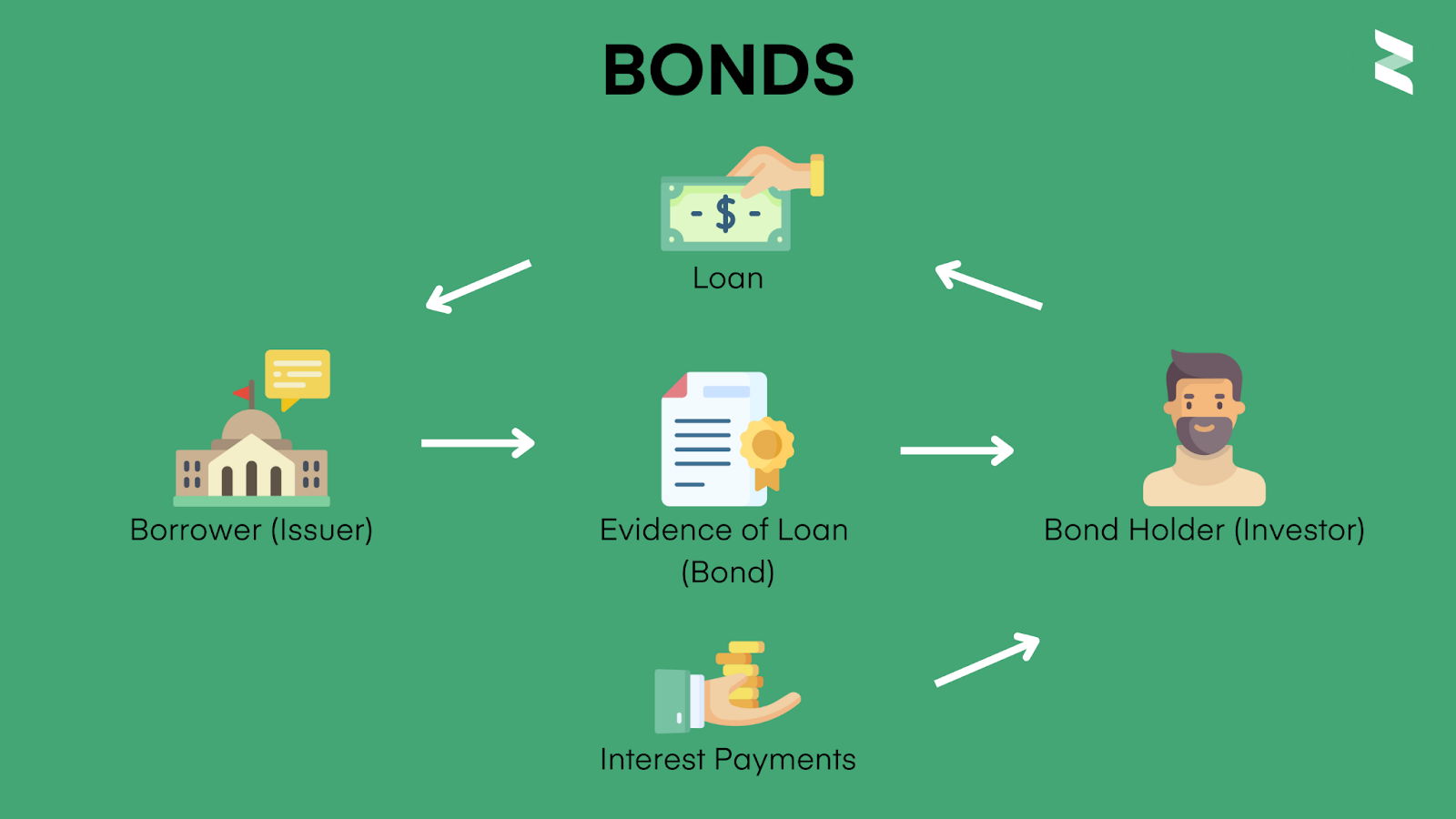

Bonds are debt-based instruments issued to investors, called bondholders, who lend their money to a borrower to receive a fixed income. Companies, governments, or states typically use bonds to finance projects and operations. Bondholders then receive coupon payments throughout the term of the bond. A big concern for Muslims is that these coupons are fixed/variable interest payments, which we can understand as an active application of riba, which, as we know, is haram.

So what can a Muslim who wants to diversify their portfolio with a more ‘stable’ asset invest in? That’s where sukuk come in - also known as the Islamic alternative to a bond.

What are sukuk?

A sukuk is an Islamic financial certificate aiming to create returns similar to conventional fixed-income instruments like bonds. Although they have seen a rise in popularity over the last twenty years, research shows that the first sukuk originated as early as the 7th century. Shell Malaysia issued the first modern-day sukuk in 1990, followed by Rantau Abang Capital Berhad's RM10 billion (U.S.$2.7 billion) issuance, which is the largest issuance size to date in the Malaysian market. With over $700 billion of assets managed according to Islamic investment principles to date, there is an apparent growing demand for Islamic finance solutions.

How do they work?

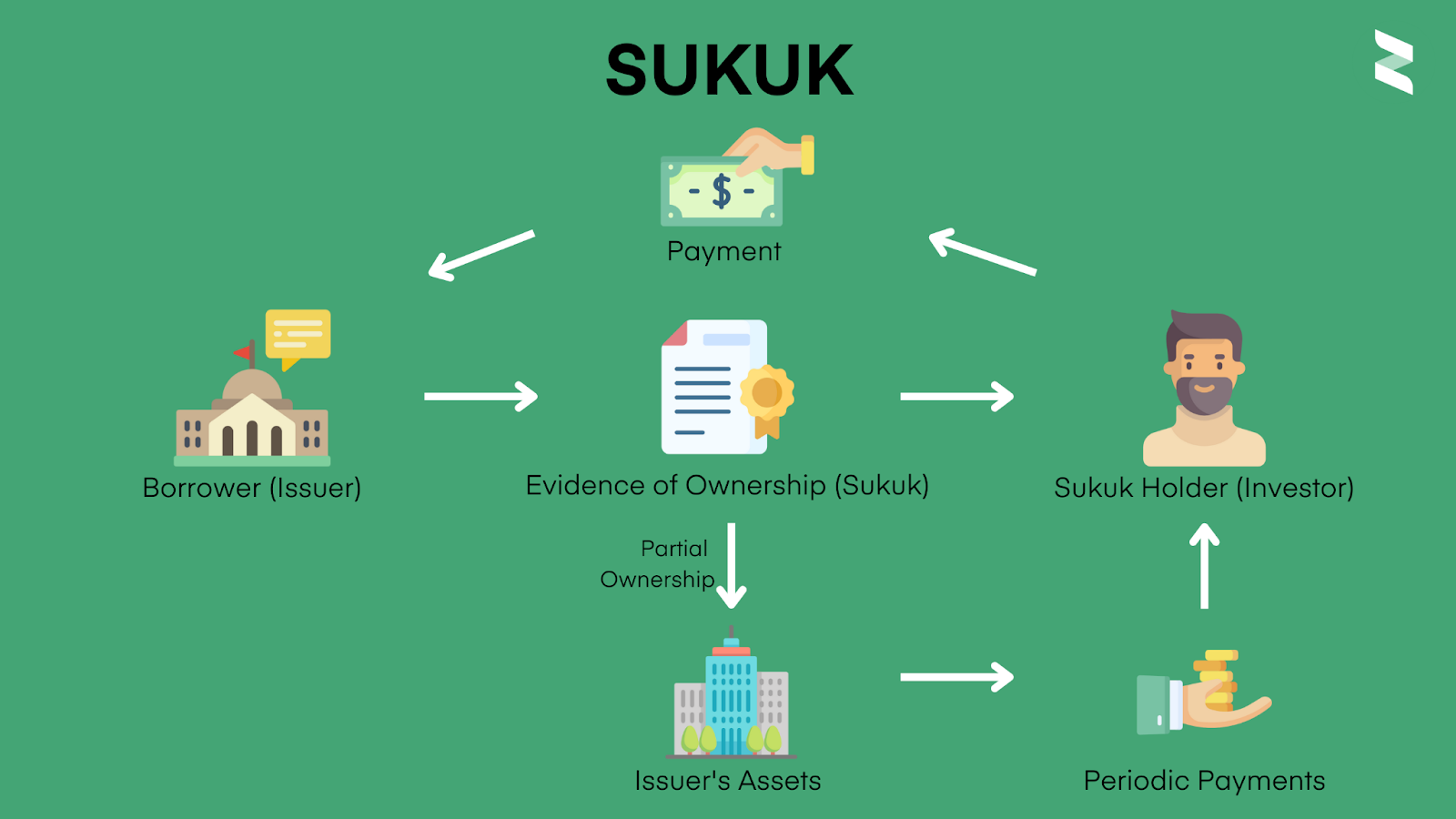

Unlike bonds, sukuk are asset-based instruments. When you invest in sukuk, your money is invested in assets that provide you with a margin of profit based on a pre-agreed ratio. Payments come in the form of profit-sharing or rental from the asset as it appreciates, and upon maturity, the sukuk holder will receive their principal investment.

How do sukuk and bonds differ?

Sukuk are a productive form of investment, allowing the sukuk holder to potentially own part of the asset, whereas bonds are a debt obligation. Sukuk payments are also linked to asset appreciation, unlike bonds that are based on an interest rate. The money raised with a sukuk is strictly used to invest in halal investments. However, bonds are riba (interest)-based and may finance haram projects.

One of the fundamental principles of Islamic finance is responsibility of risk. When investing in a sukuk, the project carries risk, and the sukuk issuer and holder take on a share of this risk. This differs from bonds, where a bondholder has no risk. The bond issuer borrows money from the bondholder, and the success or delivery of the project has no bearing on payments to the bondholder.

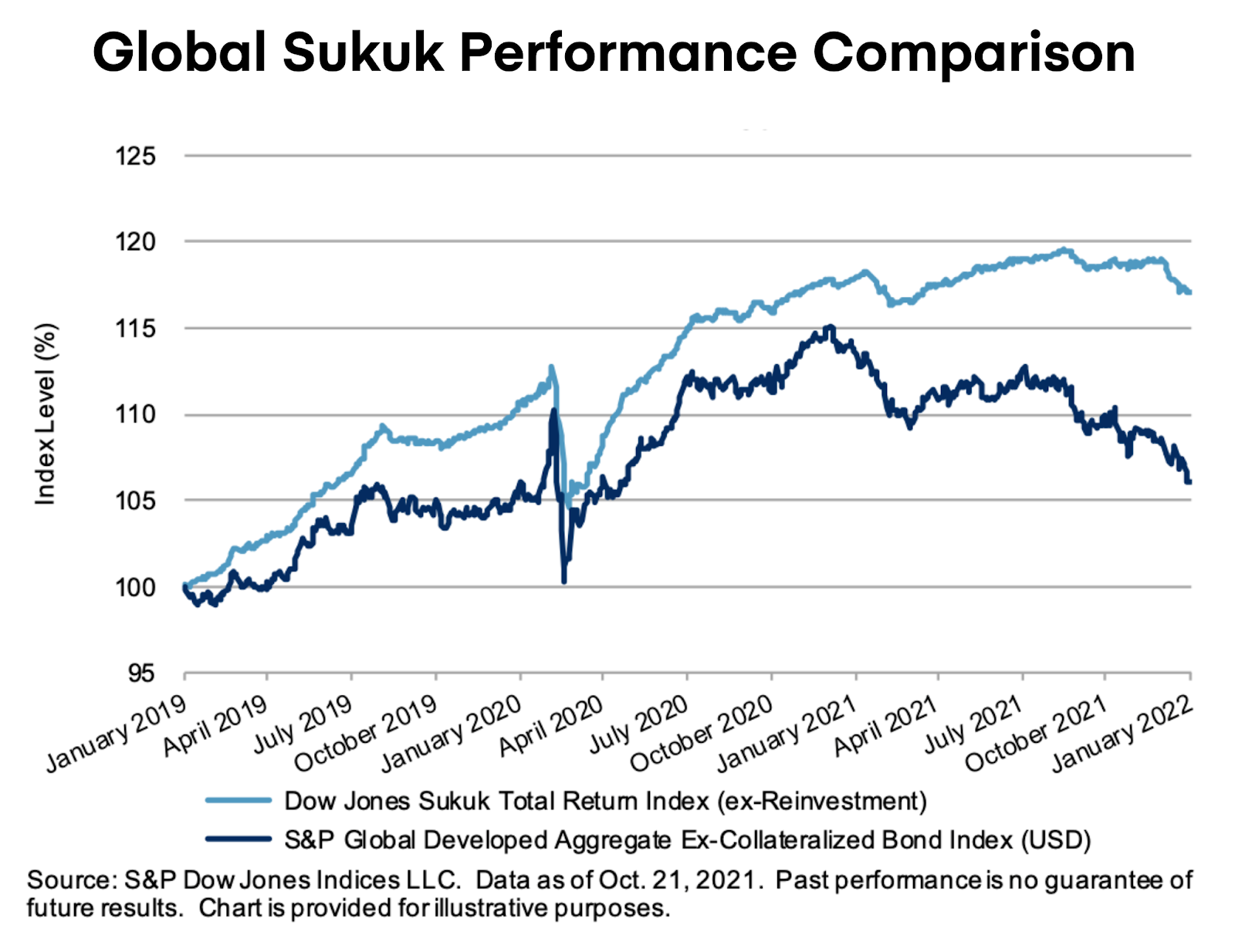

Furthermore, the chart below compares the Dow Jones Sukuk Total Return index with the S&P Global Developed Aggregate Bond index over the last three years. You can see that the sukuk index has continuously outperformed the bond index. With the increased awareness around ESG and ethical investing, ethical investors who want to diversify their assets are likely to start including sukuk in their portfolios as it is a more ethical alternative to a bond.

Different types of sukuk

Ijarah (Lease)

These are the most common form of sukuk. An Ijarah sale involves a party purchasing and leasing a specific asset for a rental fee. The duration of rental and fee is agreed upon between the sukuk issuer and the sukuk holder. The rental payments, which consist of the principal and any profit, are the source of returns for the sukuk holder.

Musharakah (Profit & Loss Sharing Partnership)

The structure of Musharakah consists of two or more parties financing a project. A pre-agreed profit-sharing ratio is distributed to all parties, and any loss is shared based on the amount contributed by each party.

Murabaha (Cost-Plus-Profit Margin Sale)

This kind of sukuk is a certificate of equal value issued to finance the purchase of goods through a sales contract where goods are sold at a price that includes the purchase price plus an agreed profit margin. The Murabaha contract is commonly used as a short-term financing instrument.

Salam (Forward Sale)

Salam is a forward sale of specified goods that will be delivered to the purchaser on a fixed date in the future in return for advanced payment, typically paid on the spot. This type of sale is an exemption to the general rules of trade which require the goods to exist at the time of sale contract. Salam sukuk utilizes the capital so that the goods can be delivered upon a specified date. These types of contracts are commonly used in the agricultural sector.

Istisna’a (Construction/Manufacturing Financing)

This type of sale involves the sale of a specified asset, with the seller obligated to manufacture or construct it and to deliver it on a specified date in return for a specific price. Istisna’a sukuk are tradable only after delivery.

Mudaraba (Profit Sharing & Loss Bearing Partnership)

Mudaraba is a partnership involving an investor and an entrepreneur, where the investor funds the enterprise or activity which the entrepreneur manages. Profits are distributed based on a pre-agreed ratio, while the investor bears any losses. These types of sukuk are typically used for encouraging public participation in large investment projects.

Why invest in sukuk?

So we know sukuk are halal to invest in, but what makes them a good investment?

They can be an excellent way to diversify your portfolio

Similar to investing in bonds, sukuk are diversified and attractively priced instruments with stable returns. Including them in your portfolio can help to reduce volatility and overall portfolio risk.

Sukuk are an alternative investment

They provide an alternative source of funding for developmental and expansion projects. Investing in a sukuk has a social and ethical benefit to the broader society.

A productive form of investment

Unlike bonds, sukuk ensure that every financial activity is backed by real economic activity, thus promoting monetary stability and real economic development.

Easy to liquidate

Sukuk are tradeable by nature, allowing investors to liquidate their investments easily whenever the need arises and, as a result, enhance market liquidity.

Common criticisms of sukuk

We’ve talked about the advantages of investing in sukuk. However, for you to make an informative decision, let’s go through some common concerns when investing in this bond alternative.

Sukuk are taxed differently

Tax treatment of sukuk can differ from conventional bonds in certain jurisdictions. Be sure to check with your local and federal tax codes before investing in a new financial instrument.

Financial risks

As with most financial instruments, sukuk are subject to rate of return risk, market risk, foreign exchange risk, and credit risk.

Returns are not fixed

Unlike bonds that have a fixed interest rate, sukuk generate returns based on the value of the assets they are invested in. This means that returns can fluctuate.

Sukuk, like bonds, use conventional finance terms such as coupon rate

A coupon is the interest payment received by a bondholder. There is a misconception that sukuk then pay interest. However, the term coupon rate, when used for sukuk refers to the expected profit rate as opposed to the interest rate.

Default risk

Default risk is related to whether the issuer pays back the investment to the sukuk holder. In contrast to bonds, sukuk claim to be a safer option as the sukuk holder has partial ownership of the asset, which will act as a security in case of default. More on the default risk of sukuk here.

Sukuk are debt instruments

In practice, not all assets that back Ijarah sukuk are targeted for leasing activities, and some Ijarah sukuk are backed by debt assets such as Murabaha and Istina’a sukuk.

Commonly misused by other practices

Ijarah contracts can sometimes be misused by using the LIBOR rate instead of adopting a rate of return following Shariah principles.

How can you invest in sukuk?

If you are interested in potentially investing in sukuk, the first step is educating yourself. You can research which sukuk funds or individual sukuk are available in your location. This may involve checking with your brokerage to see what options they offer. You can also look into resources like the Islamic Finance Foundation to stay up-to-date on news and information related to sukuk.

It's important to thoroughly research any investment you are considering, including the risks and expected returns. If you decide you want to invest in sukuk, you would need to choose a brokerage or robo-advisor platform that provides access to them. As with any investment, you should carefully weigh how sukuk fit into your financial goals and risk tolerance. Investing in sukuk or any other instrument has risks, so be sure to do your due diligence. The key is making informed decisions through your own research and analysis.

To sum up

Sukuk are halal alternatives to bonds (asset ownership vs. debt obligation). It’s essential to do your own research when it comes to investing, which also holds true with investing in sukuk. If you are looking to diversify your portfolio or bring in a more stable income, sukuk can be a great investment option. You can choose to invest in sukuk funds or individual sukuk - check your broker to see which are available based on your location.

Halal Stock Screener & Portfolio Tracker

Zoya, şeriata uygun bir yatırım portföyünü güven ve netlikle oluşturmanıza ve izlemenize yardımcı olarak helal yatırımı kolaylaştırır.